Brazil.

Brazil ranked 12th globally with an average total score of 43.

In Brazil, the first pillar consists of two schemes. The RGPS is a mandatory, pay-as-you-go-financed scheme, and it covers the private-sector workforce. The RPPS includes multiple pension schemes at different governmental levels covering public sector employees. In general, these pension plans are financed on a pay-as-you-go basis with the employee paying a percentage of their salary.

Employer sponsored pensions have a long history in Brazil and the country has the oldest system in Latin America. Two pension vehicles exist that can be used to finance private pension benefits. Closed private pension entities are non-profit organisations that can be established on a single-employer or multi-employer basis and by labor unions. Authorised financial institutions also provide pensions through open private pension entities. The closed approach is typically chosen by large employers whereas the open approach is mostly chosen by small and medium-sized employers and offered to their employees. Closed funds, sponsored mainly by large private companies, traditionally provided defined benefit pensions. Like many other countries, some of these DB plans are now closed and DC plans are on the rise.

Overall Factor Ranking

Cost

Governance

Performance

Responsible Investment

Brazil.

Brazil ranked 12th globally overall with an overall average country score of 43. The range of overall scores across funds was fairly narrow: from 34 to 52. Brazil scored in the bottom quartile of countries on three factors: governance and organisation, performance and responsible investing. In contrast, cost disclosures were relatively good and Brazil ranked in the top half of country scores.

Cost

With an average cost factor score of 57, Brazil’s ranked in the top-half with a global ranking of 6th. Individual scores ranged from 38 to 70. Detailed cost information was typically provided for ‘administrative costs’ which included investment management costs to varying degrees. Some funds only included ‘inhouse’ investment costs in financial statements but disclosed outsourced amounts in a schedule. As for all funds, marks were awarded for cost disclosures outside of the financial statements. But best practice is to include all costs in financial statements.

Governance

The Brazilian funds did not do well on this factor with an average overall score of 43 and a global ranking of 12th. The range of overall scores was remarkably tight: from a low of 40 to a high of 45. Disclosures for governance structure and mission were an area of relative strength and the Brazilian funds were about median on this component. In contrast, compensation, HR and organisational disclosures were a particular weak spot. Brazil was one of three countries where none of the funds disclosed board compensation. More Brazilian funds discussed desired board member competencies than in any other country. Unfortunately, the funds discussed what was desired, but did not disclose the actual competencies of their current board members.

Performance

The Brazilian funds did poorly on the performance factor with a country ranking of 15th and the lowest average country score of 51. Individual fund scores ranged from 35 to 67. Key performance components that scored poorly relative to other countries included: total fund/investment option and asset class return and value added reporting; benchmark clarity and quality; clarity for basis of return and value added disclosures, and risk management policies and practices.

Responsible Investment

The Brazilian funds also did relatively poorly on the responsible investing factor, with an average country score of 19 and a global ranking of 13th. Individual fund RI scores ranged from 8 to 27. RI implementation was the weakest component, especially related to active ownership and impact investing – disclosures were either minimal and most often missing. Scores were generally more mid-range for RI framework and reporting.

Example

Petros

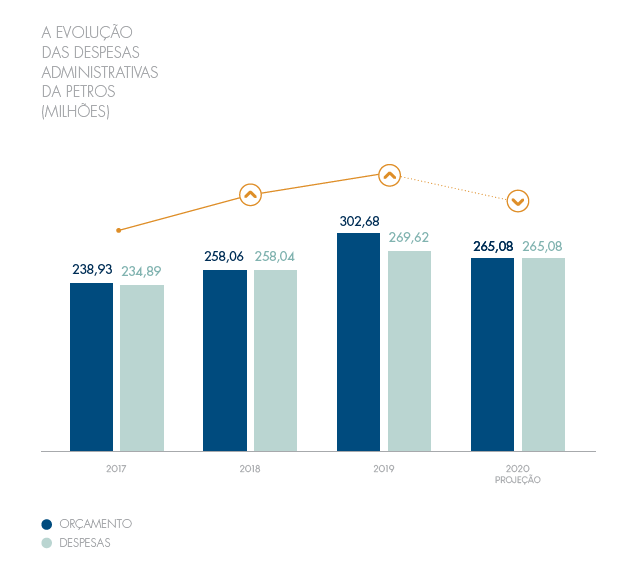

The Petros Annual Report discusses the budget for the current year relative to actual expenditure as well as the budget for the next year.

Resource optimisation: Policy and cost reduction

Petros’ resource optimisation and cost reduction policy intensified in 2019. At the end of the year, administrative expenses were R$269.62 million, which represents an 11% reduction compared to the R$302.68 million that had been initially estimated for the 2019 budget. For 2020, the budget is foreseen in R$265.08 million. The amount represents a decrease of 12.4% in compared to the budget initially projected for 2019 and also 1.7% compared to expenses actually incurred, ensuring control of spending. The economy is the result of a series of actions to ensure more efficiency.

In resource management, reducing Petros costs and ensuring equity of the participants. A successful strategy has been an intense negotiation of new service contracts services, renovations and additives. This has ensured, on average, a reduction in 5% in the cost of contracts. In addition, there are periodic contractual renegotiation, in which new opportunities are assessed cost cuts.

In recent years, the Foundation has increased control over the use of resources. Orderly control mechanisms have been implemented budget – creation of a reserve fund, based on surplus budgets and establishing limits of value and hierarchy for allocation of funds – and requirements for hiring. In 2019, Petros also reduced expenses that were planned with travel and training of its employees.

Petros compares budget and actual and projected administration expenses

Source: Petros Annual Report 2019 (page 76 and 69) – translated to English

Overall Results

Brazil.

Funds Analysed

Funcef

Funcef is the third largest pension fund in the country, with more than R$70 billion in assets and 135,000 participants. Its members are employees of CAIXA, a Brazilian bank that is the largest 100% government-owned financial institution in Latin America.

Itau Unibanco

Itau Unibanco provides a number of pension schemes for its employees and for subsidiary companies. Itau Unibanco is the largest private sector bank in Brazil and the largest in Latin America. It has operations in eight countries in the Americas as well as eight other countries.

Petros

Petros is a pension entity created by Petrobas, the national oil company. It has legacy DB plans for Petrobas and subsidiary companies, newer DC plans for them, and it now offers pension plan services for other employers and organisations in Brazil.

Previ

Previ has a long history, dating back to 1904. It is now among the largest pension funds in Latin America. Previ is the pension fund for employees of Banco do Brasil, and its own employees. There are two main plans: a DB scheme that has been closed to new entrants for some time, and a newer, open DC plan – Previ Futuro.

Vivest

Vivest was known as Funcesp until recently and it started as a provider of pension and health benefit programs for CESP, a large electricity generation company in the State of São Paulo. Today, Vivest is the largest private pension fund in Brazil.