Chile.

Chile ranked 12th globally with an average total score of 45.

In 1981, Chile introduced a mandatory defined contribution pension system. Employees are required to contribute 10 per cent of their salary and choose a private Pension Fund Administrator (AFP). AFPs are chartered as pension providers by the Chilean government and compete for individual accounts. This pension system has become known as the ‘Chilean Model’ and versions of it have been implemented in other Latin American countries. The public disclosures of the largest Chilean private sector Pension Fund Administrators (AFPs) were reviewed.

AFP investment programs are dictated by regulation. AFPs are allowed to offer up to five investment funds, called Funds A to E, which have different proportions of their portfolios invested in equities. All AFPs must offer funds B to E, while fund A, the highest equity/highest risk fund is optional. All funds operate within regulated investment limits that cover investments in various asset classes and investment vehicles. AFPs must meet a minimum level of return for each fund that is tied to the average return for all funds of that type. There is a guarantee obligation that requires AFPs to top-up their underperforming funds. Not surprisingly, most AFPs invest in a similar way to ensure they are not required to inject capital into their funds.

AFPs set the administration fees they charge members, but the fee must be the same percentage of salary for all their members. These fees are known as commission and are applied to contributions into the funds. Commissions are intended to cover all AFP costs and generate a profit margin.

Overall Factor Ranking

Cost

Governance

Performance

Responsible Investment

Chile.

Chile was one of two countries that saw its rankings improve by two places, moving from 14th place to 12th. The improvement in ranking was down to much improved cost disclosures where the Chilean AFP’s moved from being the 12th ranked country to 4th place, an impressive improvement. Governance disclosures also improved slightly, while performance and RI disclosures continued to be lacking. AFP websites were focused on engaging with members and attracting new business and were generally appealing. However, disclosures for many of the transparency elements in the benchmark were often missing or minimal, both on websites and in public documents like annual reports. Most AFPs are part of larger commercial organisations. Only disclosures specific to the AFPs themselves were scored. Disclosures of parent companies were not scored.

Cost

Chile ranked 4th globally with a cost factor score of 56. These results are in stark contrast with last year, where Chile ranked 12th. The spread is narrowly banded, with a low of 47 and a high of 63. The change in score is a result of improvements across all reviewed cost components, except for member service cost disclosures, which were materially similar. Notably, all AFPs have significantly improved both their asset class level disclosures as well as the completeness of their external management fee disclosures.

Governance

Overall, there was little year-over-year change in governance disclosures for the AFPs. Despite an increase in average score to 60, the global ranking of Chilean funds slipped to 10th, down one place from last year’s ranking. The range in scores was quite wide: from a low of 46 to a high of 72. Organisational strategy disclosures saw the largest improvement. In many cases it was necessary to review several different documents in order to find information. Information could be summarised in a more cohesive and useful format.

Performance

Unlike cost disclosures, performance disclosures were largely unchanged from last year’s review. An average score of 55 meant that Chilean AFPs continued to rank 13th globally. Disclosures of investment option returns and value added continued to uniformly complete and presented with great clarity. Much of this reporting was found on the regulator’s website. Disclosure of asset class performance and benchmarks as well as risk continued to be poor.

Responsible Investment

While disclosures in this area did improve somewhat from last year’s review, RI continued to be a weak spot for the Chilean AFPs. The average score was 11 and their global rank slipped one place to 15th. Scores were low for all RI components, though there were some minor improvements in areas such as impact investing and RI framework.

Example

AFP

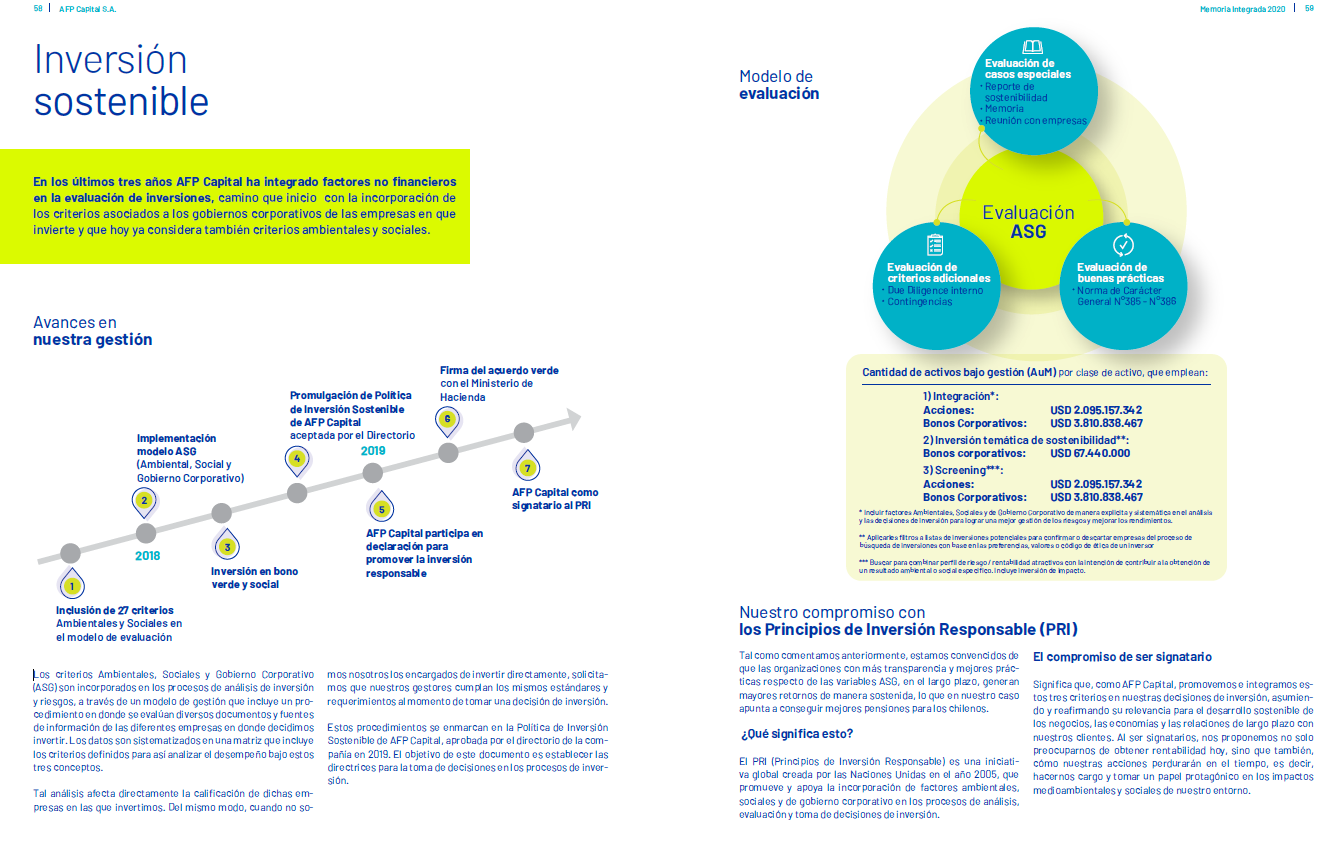

While RI disclosures in Chile were generally lacking, Capital AFP which utilizes the <IR> framework provided this insightful disclosure on the progress of its ESG investment program and an overview of how it evaluates the program.

Source: Capital AFP, Integrated Annual Report, pg. 58-59

Overall Results

Chile.

Funds Analysed

Capital

Capital is an AFP that is part of Grupo SURA, a Colombian company that offers pension fund management and other financial services in Chile and several other Latin American countries.

Cuprum

Cuprum is an AFP with more than 35 years of history in the Chilean pension system and its inception is tied to the copper mining sector. Cuprum is now part of the Principal Financial Group, a large global financial services company headquartered in the United States.

Habitat

Habitat is the second largest Chilean AFP by assets under management. It also owns pension fund management companies in Peru and Colombia. In 2016, Prudential Financial, a large US global financial services company purchased an interest in Habitat.

Modelo

Modelo is a relatively new domestically owned AFP. It commenced operations in 2010 and has grown quickly.

Provida

Provida was founded in 1981 and is the largest Chilean AFP by assets under management. Provida is now part of MetLife, a large US global financial services company.