Countries

Promoting transparency for better pension outcomes

Select country to see results

Australia.

Australia ranked 4th globally with an average total score of 65.

The first pillar of Australia’s pension system is a means-tested, unfunded age-based pension that provides a basic benefit. The backbone of the country’s pension system is the second pillar, a mandatory defined contribution system with minimum required contributions for all workers which was introduced in 1992. Before the compulsory superannuation system was introduced, defined benefit schemes were the more popular form of occupational pension provision. The environment is competitive as individuals select the superannuation fund for their contributions. There are many superannuation providers which generally fall into two categories: not-for-profit industry funds and retail funds, which are offered to the public by financial services companies.

Overall Factor Ranking

Cost

Governance

Performance

Responsible Investment

Australia.

Cost

With an average cost factor score of 67, Australia’s superannuation funds ranked 3rd globally. Individual scores ranged from 58 to 84. Four of the funds offer DC options in a competitive environment, so the questions relating to completeness of external management and transaction costs were all from the perspective of product disclosure statements to members. Some of the Australian funds did a very good job of including all transaction costs (including implicit ones like market impact, buy and sell spreads, etc.) and quantifying and disclosing this to members. Commendable and not typical relative to funds globally.

Governance

The Australian funds did very well on this factor with an average score of 72, second behind Canada. The range of scores was quite narrow: from a low of 65 to a high of 80. Funds scored well in all areas except organisational strategy, which was a surprise since all super funds are fully integrated investment management and member service organisations. Members would benefit from a clearer picture of where their super fund is heading. Where the Australian funds did particularly well was in disclosures on compensation, human resources and organisation, receiving the top grade in this area. Compensation disclosures for both the board and management were especially impressive – all funds received top marks.

Performance

The Australian funds scored well in performance with an average country score of 76 and a global ranking of 4th on the factor. Scores were quite consistent across funds, ranging in a narrow band from 66 to 86. Scores on most performance components were around the top-quartile mark with two outliers. Benchmark disclosures were relatively weak at the asset class level. In contrast, the Australians had the highest average score on disclosures for member service levels. It seems the competitive environment and freedom that individuals enjoy to switch funds drives more emphasis on member service.

Responsible Investing

The Australian funds had an average country score of 46 on RI and ranked 8th globally. Individual fund scores ranged widely from a low of 8 to a high of 70. Areas of relative strength were: active ownership policies, ranked 4th with an average score of 72, and exclusion policies and practices ranked 4th with an average score of 70. Disclosures in other areas were generally mid-range relative to other countries.

Examples

AustralianSuper

Source: AustralianSuper website

Source: AustralianSuper websiteFirst State Super

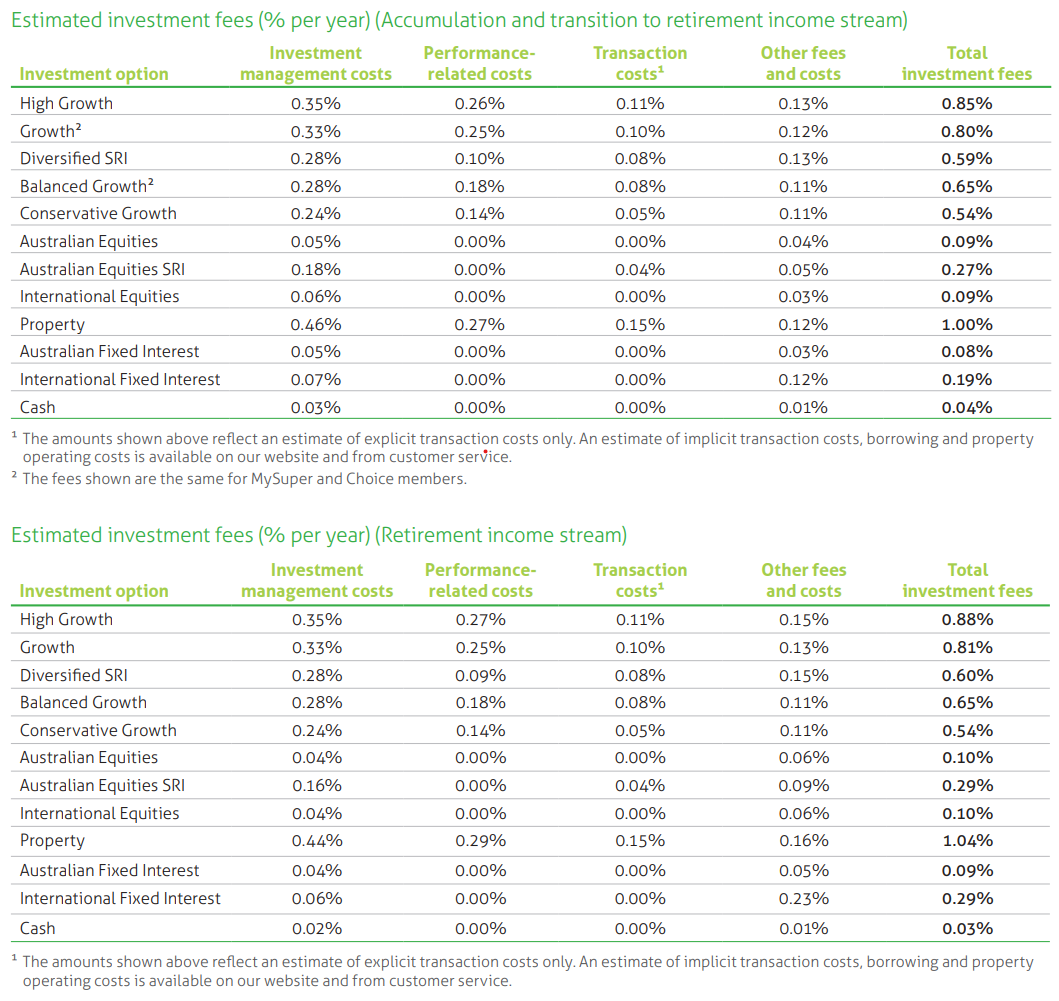

First State Super has a very good breakdown of the estimated investment fees annually by investment option. This annual report was produced in 2019 prior to the merger and name change to AwareSuper.

Source: First State Super Annual Report 2019 (page 16)

Overall Results

Australia.

Funds Analysed

AustralianSuper

AustralianSuper is the largest Australian superannuation and pension fund, with approximately one in every 10 Australian workers as members. It is a not-for-profit industry superannuation fund.

Aware Super

Aware Super is a not-for-profit industry fund with a new name but a history going back to 1992. It is Australia’s second largest fund, with $130 billion under management following the merger between First State Super and VicSuper.

Future Fund

Future Fund is an independently managed sovereign wealth fund established in 2006 to meet unfunded public sector superannuation liabilities.

QSuper

QSuper is an Australian superannuation fund based in Brisbane, Queensland. The fund was established in 1912 through an Act of Parliament. It is a not-for-profit fund, with around 585,000 members and $113 billion.

UniSuper

UniSuper is a not-for-profit superannuation fund with origins as a provider of superannuation for employees of Australia’s higher education and research sector.

Brazil.

Brazil ranked 12th globally with an average total score of 43.

In Brazil, the first pillar consists of two schemes. The RGPS is a mandatory, pay-as-you-go-financed scheme, and it covers the private-sector workforce. The RPPS includes multiple pension schemes at different governmental levels covering public sector employees. In general, these pension plans are financed on a pay-as-you-go basis with the employee paying a percentage of their salary.

Employer sponsored pensions have a long history in Brazil and the country has the oldest system in Latin America. Two pension vehicles exist that can be used to finance private pension benefits. Closed private pension entities are non-profit organisations that can be established on a single-employer or multi-employer basis and by labor unions. Authorised financial institutions also provide pensions through open private pension entities. The closed approach is typically chosen by large employers whereas the open approach is mostly chosen by small and medium-sized employers and offered to their employees. Closed funds, sponsored mainly by large private companies, traditionally provided defined benefit pensions. Like many other countries, some of these DB plans are now closed and DC plans are on the rise.

Overall Factor Ranking

Cost

Governance

Performance

Responsible Investment

Brazil.

Brazil ranked 12th globally overall with an overall average country score of 43. The range of overall scores across funds was fairly narrow: from 34 to 52. Brazil scored in the bottom quartile of countries on three factors: governance and organisation, performance and responsible investing. In contrast, cost disclosures were relatively good and Brazil ranked in the top half of country scores.

Cost

With an average cost factor score of 57, Brazil’s ranked in the top-half with a global ranking of 6th. Individual scores ranged from 38 to 70. Detailed cost information was typically provided for ‘administrative costs’ which included investment management costs to varying degrees. Some funds only included ‘inhouse’ investment costs in financial statements but disclosed outsourced amounts in a schedule. As for all funds, marks were awarded for cost disclosures outside of the financial statements. But best practice is to include all costs in financial statements.

Governance

The Brazilian funds did not do well on this factor with an average overall score of 43 and a global ranking of 12th. The range of overall scores was remarkably tight: from a low of 40 to a high of 45. Disclosures for governance structure and mission were an area of relative strength and the Brazilian funds were about median on this component. In contrast, compensation, HR and organisational disclosures were a particular weak spot. Brazil was one of three countries where none of the funds disclosed board compensation. More Brazilian funds discussed desired board member competencies than in any other country. Unfortunately, the funds discussed what was desired, but did not disclose the actual competencies of their current board members.

Performance

The Brazilian funds did poorly on the performance factor with a country ranking of 15th and the lowest average country score of 51. Individual fund scores ranged from 35 to 67. Key performance components that scored poorly relative to other countries included: total fund/investment option and asset class return and value added reporting; benchmark clarity and quality; clarity for basis of return and value added disclosures, and risk management policies and practices.

Responsible Investment

The Brazilian funds also did relatively poorly on the responsible investing factor, with an average country score of 19 and a global ranking of 13th. Individual fund RI scores ranged from 8 to 27. RI implementation was the weakest component, especially related to active ownership and impact investing – disclosures were either minimal and most often missing. Scores were generally more mid-range for RI framework and reporting.

Example

Petros

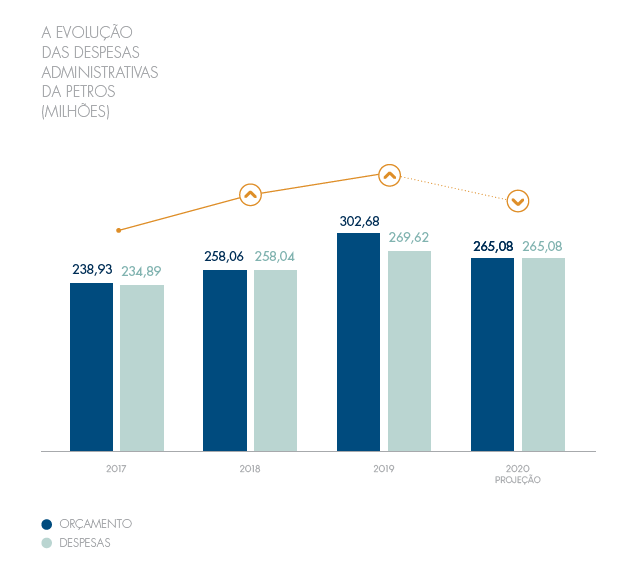

The Petros Annual Report discusses the budget for the current year relative to actual expenditure as well as the budget for the next year.

Resource optimisation: Policy and cost reduction

Petros’ resource optimisation and cost reduction policy intensified in 2019. At the end of the year, administrative expenses were R$269.62 million, which represents an 11% reduction compared to the R$302.68 million that had been initially estimated for the 2019 budget. For 2020, the budget is foreseen in R$265.08 million. The amount represents a decrease of 12.4% in compared to the budget initially projected for 2019 and also 1.7% compared to expenses actually incurred, ensuring control of spending. The economy is the result of a series of actions to ensure more efficiency.

In resource management, reducing Petros costs and ensuring equity of the participants. A successful strategy has been an intense negotiation of new service contracts services, renovations and additives. This has ensured, on average, a reduction in 5% in the cost of contracts. In addition, there are periodic contractual renegotiation, in which new opportunities are assessed cost cuts.

In recent years, the Foundation has increased control over the use of resources. Orderly control mechanisms have been implemented budget – creation of a reserve fund, based on surplus budgets and establishing limits of value and hierarchy for allocation of funds – and requirements for hiring. In 2019, Petros also reduced expenses that were planned with travel and training of its employees.

Petros compares budget and actual and projected administration expenses

Source: Petros Annual Report 2019 (page 76 and 69) – translated to English

Overall Results

Brazil.

Funds Analysed

Funcef

Funcef is the third largest pension fund in the country, with more than R$70 billion in assets and 135,000 participants. Its members are employees of CAIXA, a Brazilian bank that is the largest 100% government-owned financial institution in Latin America.

Itau Unibanco

Itau Unibanco provides a number of pension schemes for its employees and for subsidiary companies. Itau Unibanco is the largest private sector bank in Brazil and the largest in Latin America. It has operations in eight countries in the Americas as well as eight other countries.

Petros

Petros is a pension entity created by Petrobas, the national oil company. It has legacy DB plans for Petrobas and subsidiary companies, newer DC plans for them, and it now offers pension plan services for other employers and organisations in Brazil.

Previ

Previ has a long history, dating back to 1904. It is now among the largest pension funds in Latin America. Previ is the pension fund for employees of Banco do Brasil, and its own employees. There are two main plans: a DB scheme that has been closed to new entrants for some time, and a newer, open DC plan – Previ Futuro.

Vivest

Vivest was known as Funcesp until recently and it started as a provider of pension and health benefit programs for CESP, a large electricity generation company in the State of São Paulo. Today, Vivest is the largest private pension fund in Brazil.

Canada.

Canada ranked 1st globally with an average total score of 74.

Canada’s pension system is characterised by a mixture of public and private pension schemes. Approximately half of all Canadians rely on the public pension system which consists of two tiers: 1. Old age security – set amounts paid to all Canadians of retirement age, based solely on residency 2. Canada Pension Plan (CPP) – a mandatory earnings related pension covering all workers. The third tier of Canada’s pension system is made up of voluntary pension savings. Defined benefit plans remain the most common type of scheme in Canada, particularly for public sector employees. Like many other countries, defined contribution plans are now the plan of choice for private sector employers. The public disclosures of the CPP and four organisations that manage mainly DB plan assets for provincial public sector employers were reviewed.

Overall Factor Ranking

Cost

Governance

Performance

Responsible Investment

Canada.

Canadian funds had impressive public disclosures. They ranked 1st globally with an average total score of 74. By factor they ranked: 1st in governance; 2nd for performance; 2nd for cost; and 4th in responsible investing.

Most of what was scored focused on ‘what’ was disclosed. Canadian funds also excelled on communication dimensions that were not scored. Their annual reports were well organised, cohesive and packed with important information for stakeholders. The narratives typically went beyond just ‘what we do’ to add insights about ‘how we do things’ and ‘why we do it this way’. They also realise that less can be more, making good use of infographics, summaries, pictures, charts, etc., and less text, to add impact and keep readers engaged.

Cost

The average score for cost disclosure was 69 and scores for funds ranged from a low of 59 to a high of 83. Disclosures were consistently good for total fund level and for external manager fees. Asset class and transaction cost disclosures were inconsistent across the funds and scored low on average.

Governance

The biggest Canadian public funds collectively have a global reputation for superior performance and governance excellence is often cited as a key driver (the Maple Model). The CEM benchmarking database provides empirical evidence that the Maple Model funds do indeed outperform over the long term. The #1 governance ranking and average score of 86 for the five largest Canadian funds also supports their collective reputation for governance excellence. From many, two examples that illustrate Canadian governance best practices in action have been selected.

Performance

With an average score of 84, Canadian funds ranked 2nd globally and generally scored consistently well across the various components. Risk, asset mix and portfolio composition, as well as total fund return and value add disclosure were especially good. Canadian funds also typically provided clear and detailed disclosures of the basis for their return and valued added reporting. Returns were explicitly stated as time-weighted for the total fund and most asset classes and occasionally as IRR for private market asset classes. Total fund returns were consistently and explicitly stated as net of all investment costs and the cost basis for asset class returns was clear. Surprisingly, this level of detail for returns and value added was not universal. Return basis disclosures were often cryptic or non-existent. This makes understanding and comparing results across funds very difficult.

Responsible Investment

Canadian funds had an average RI factor score of 58. RI component scores varied widely across the funds. The weakest area overall for this factor was governance. For implementation, active ownership disclosures were consistently very good, while exclusion policy disclosures were consistently very low.

Examples

PSP Investments

PSP Investments provides an excellent overview of its governance mission, structure and processes as well as director qualifications, competencies, performance and compensation. Here are selected excerpts from the governance section of its annual report.

Board responsibilities

In accordance with the Act, the Board of Directors manages or supervises the management of the business and affairs of PSP Investments. In discharging their duties, Directors are required to act honestly and in good faith with a view to the best interests of PSP Investments, and to exercise the care, diligence and skill that a reasonable person would exercise in comparable circumstances. The Board performs three vital functions:

• Decision-making—the Act provides for a number of decisions that cannot be delegated to management.

• Where appropriate, the Board makes such decisions with advice from management.

• Oversight—supervising management and overseeing risks.

• Insight—advising management on matters such as markets, strategy, stakeholder relations, human resources and negotiating tactics.

The Board’s specific responsibilities include:

• Determining the organization’s strategic direction in collaboration with senior management;Selecting and appointing the President and CEO and annually reviewing his or her performance;

• Reviewing and approving the Statement of Investment Policies, Standards and Procedures (SIP&P) for each pension plan on an annual basis;

• Ensuring that risks are properly identified, evaluated, managed, monitored and reported; Approving benchmarks for measuring investment performance;

• Establishing and monitoring compliance with PSP Investments’ Code of Conduct;

• Approving human resources and compensation policies related to attracting, developing, rewarding and retaining PSP Investments’ talent;

• Establishing appropriate performance evaluation processes for Board members, the President and CEO, and other senior management members;

• Approving quarterly and annual financial statements for each pension plan and for PSP Investments as a whole; and Establishing Terms of Reference for the Board, Board committees, and Board and committee chairs.

Director appointment process

Director appointment process Directors are appointed by the Governor in Council on the recommendation of the President of the Treasury Board of Canada for terms of up to four years. When their term expires, they may be reappointed for an additional term or continue in office until a successor is appointed. Candidates are selected from a list of qualified Canadian residents proposed by an external nominating committee established by the President of the Treasury Board of Canada. The Nominating Committee operates separately from the Board, the President of the Treasury Board of Canada and the Treasury Board Secretariat. The appointment process is designed to ensure that the Board has a full contingent of high-calibre Directors with proven financial ability and relevant work experience. The Governance Committee regularly reviews and updates desirable and actual competencies, experiences and attributes to ensure that decisions are made with a view to having a diverse Board that can provide the oversight and guidance needed for PSP Investments to fulfill its mandate. Our Board currently has gender balance with women representing five out of the 11 Directors. In addition, two Directors have self-identified as belonging to a visible minority.

Director orientation and education

Director orientation and education Newly appointed Directors participate in a structured orientation program that introduces them to PSP Investments’ culture and operations, so they can contribute effectively as Board members. The Governance Committee has created a Director education program to support ongoing professional development. Through this program, Directors are allocated an education and training budget to be used primarily for taking courses, attending conferences and procuring reading material to strengthen their understanding of investment management and other relevant areas. Directors report annually on their individual development plans. On occasion, internal and outside speakers are invited to make presentations that contribute to the individual and collective expertise of Board members.

Board committees

The Board fulfills its obligations directly and through four standing committees:

Investment and Risk Committee—oversees PSP Investments’ investment and risk management functions.

Audit Committee—reviews financial statements and the adequacy and effectiveness of internal control systems, and oversees the internal audit function.

Governance Committee—monitors governance matters, develops related policies, and oversees the application of the Code of Conduct.

Human Resources and Compensation Committee— ensures policies and procedures are in place to manage the human resources function efficiently and effectively, and to offer all employees fair and competitive compensation aligned with performance and risk targets.

Fiscal year 2020 key activities

Investment and Risk Committee

• Reviewed and approved 16 investments.

• Approved changes to the Risk Appetite Statement.

• Recommended for Board approval a new custodian for PSP Investments’ assets.

• Reviewed the fund strategy of the Private Equity asset class.

• Reviewed market downturn scenarios and related stress-testing in preparation for a market downturn.

Audit Committee

• Reviewed PSP Investments’ cybersecurity and cloud strategies.

• Examined cost containment measures as part of the annual budget process and projected future costs.

• Approved the launch of the next special examination.

• Reviewed PSP Investments’ valuation procedure for private assets (this occurred post fiscal year-end).

Governance Committee

• Reviewed Board and Committee responsibilities and recommended new Terms of Reference for the Board, its committees, and the Board and committee chairs.

• Proposed enhancements to the Board evaluation process.

• Recommended for Board approval committee composition changes, including a new Chair for the Human Resources and Compensation Committee as part of the succession planning process.

• Recommended for Board approval amendments to PSP Investments’ Responsible Investment Policy and approved new Proxy Voting Principles.

• Conducted a review of Director remuneration.

Human Resources and Compensation Committee

• Conducted a full review of succession planning for the CEO and Officers.

• Recommended for Board approval a new benchmark, threshold level of performance and value-added objectives based on a total fund approach.

• Adopted a new Human Resources Policy confirming PSP Investments’ commitment to attracting, developing, rewarding and retaining our talent.

Source: PSP Annual Report 2020 (pages 49 – 54)

British Columbia Investment Management Corporation

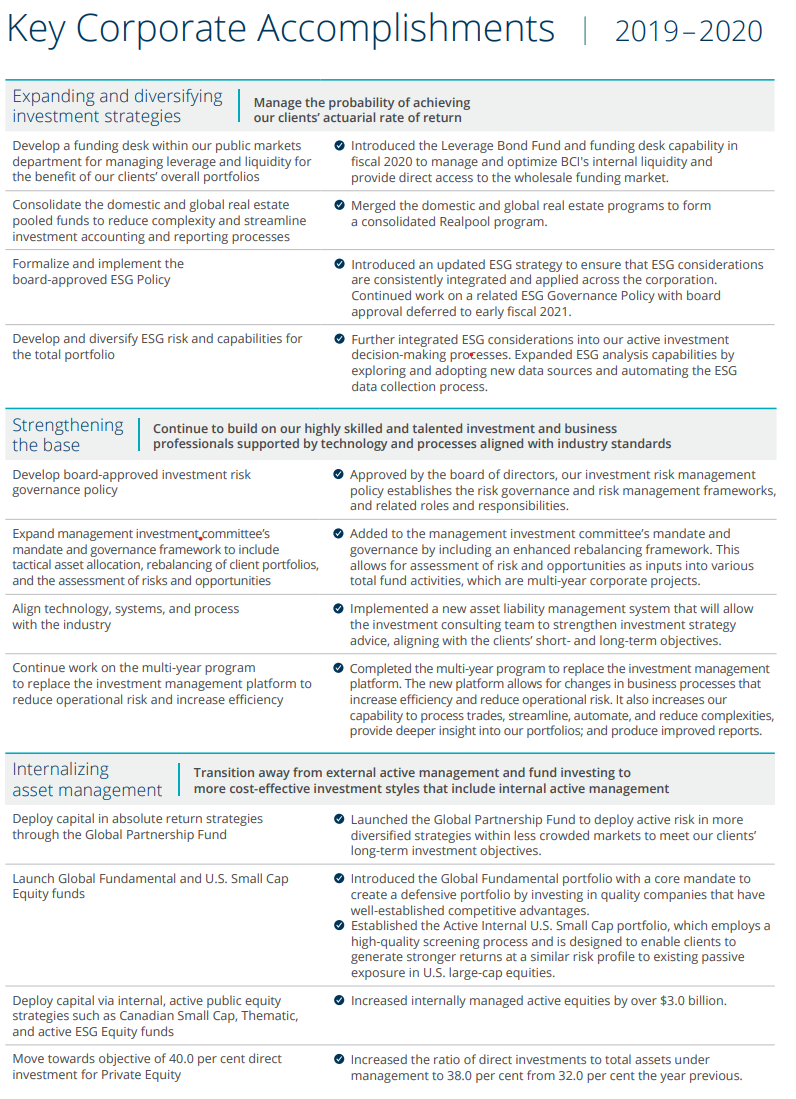

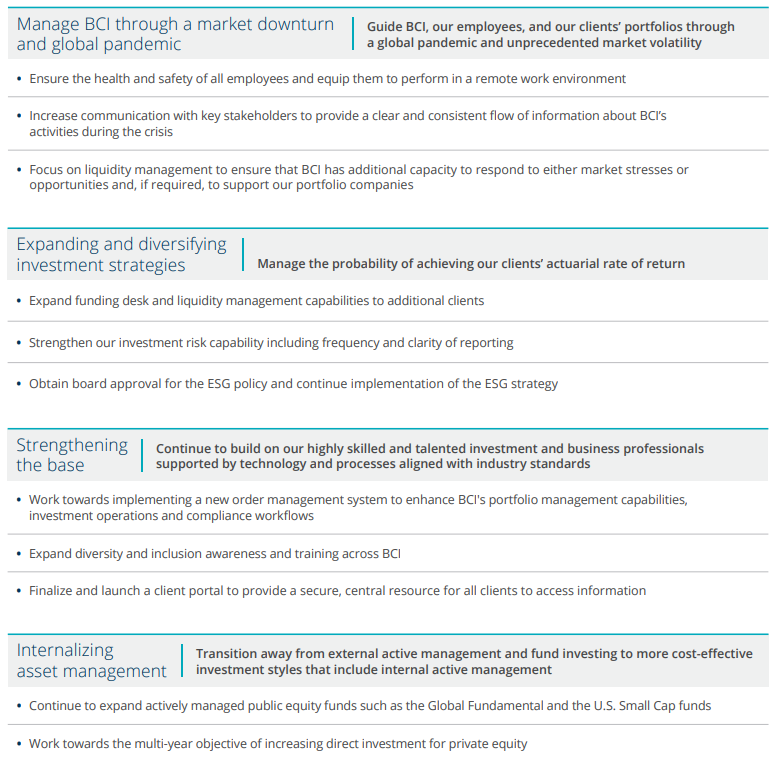

British Columbia Investment Management Corporation’s annual report includes a concise two page summary of its previously published key corporate development goals for the year, along with a progress report card. Objectives for the upcoming year are disclosed in tandem.

Source: BCI Corporate Annual Report 2019 – 2020 (pages 16 and 17)

Overall Results

Canada.

Funds Analysed

British Columbia Investment Management Corporation (BCI)

BCI manages the assets of public sector pension plans as well as insurance and benefit funds for the province of British Columbia.

Caisse de dépôt et placement du Québec (CDPQ)

CDPQ invests funds for several public and parapublic pension plans and insurance programs in the province of Quebec.

CPP Investments (CPPIB)

CPPIB manages the assets of the Canada Pension Plan, the national pension scheme for Canadian workers.

Ontario Teachers’ Pension Plan (OTPP)

OTPP is responsible for managing plan assets and administering defined-benefit pensions for school teachers in the province of Ontario.

Public Sector Pension Investment Board (PSP)

PSP invests funds for the pension plans of the Public Service, the Canadian Armed Forces, the Royal Canadian Mounted Police and the Reserve Force.

Insights

Canada marks five-year reign as global transparency leader

Canada has been named the country with the most transparent pension funds for the fifth...

Global pension funds lift transparency, but cost reporting still lags

Global asset owners have made significant advancements in the transparency of disclosures with the...

Norway’s GPFG keeps most transparent pension fund title with perfect score

Norway’s $2 trillion Government Pension Fund Global has retained its title as the world’s most...

CPP Investments, NBIM reflect on lessons from a 5-year transparency journey

The Global Pension Transparency Benchmark has been a driving force in improved transparency of disclosures and reporting among global asset owners....

Why transparency is a strategic initiative for Norway’s SWF

Norway’s giant sovereign wealth fund took out the top spot in this year’s Global Pension Transparency Benchmark. Amanda White talks to CEO of Norges...

Global Pension Transparency Benchmark makes process improvements

The Global Pension Transparency Benchmark, a collaboration between Top1000funds.com and CEM Benchmarking, ranking pension funds globally on their...

Benchmark proves scrutiny on disclosure drives transparency improvements

Now in its fourth iteration, the Global Pension Transparency Benchmark shows that ongoing scrutiny of cost, governance, performance and responsible...

Please note, your details will be shared with both CEM and Top1000funds.com. Your data will never be shared with any other organisations or third parties.

CEM Benchmarking is an independent provider of cost and performance benchmarking information for pension funds and other institutional asset owners worldwide. It believes ‘what gets measured gets managed’ and is deeply committed to helping clients run cost-effective operations that generate value for their stakeholders. With vast industry knowledge and a robust database spanning 28 years and $10+ trillion in AUM, CEM helps more than half of the world’s top 300 pension schemes understand and manage their costs and performance. CEM also facilitates better pension outcomes by sharing cutting edge research derived from its proprietary databases.

Top1000funds.com is the market leading news and analysis site for the world’s largest institutional investors. It focuses on leading the global investment industry to continuous improvement through case studies of best practice in governance and decision making, portfolio construction and efficient portfolio management, fees and costs, and sustainable investing. The publication pushes the industry to question whether status quo processes and behaviours to tackle risks and opportunities will be sufficient in the future, and actively campaigns for diversity, sustainability, transparency, innovation and better alignment of fees in the investment industry. Top1000funds.com is read by investment professionals in more than 40 countries.

Categories

Links

© 2021 Conexus Financial. Top1000funds.com. Please read our Terms and Conditions, Privacy Policy and Terms of use.